Starting a small business means making several crucial decisions right from day one. One of the most important of these is choosing the right business structure. Should you be a sole proprietor? Form an LLC? Or consider a Limited Liability Partnership (LLP)? Each has its own pros and cons. But today, we’re diving deep into a specific question: Is an LLP good for a small business?

To answer this properly, we need to understand the background of LLPs, the legal implications, the tax treatment, the pros and cons, and how LLPs compare with other structures. Let’s explore this in full detail to provide an informed and well-rounded analysis for entrepreneurs.

LLP vs LLC: Which One is Better for a Small Business?

Both LLPs and LLCs provide limited liability protection and pass-through taxation, making them popular choices for small business owners. However, the difference between LLP and LLC lies in operational flexibility and investment compatibility. LLCs are more versatile for businesses seeking capital, while LLPs are preferred in service-oriented partnerships.

LLCs have a more formal management structure and allow members to take on varying levels of responsibility, whereas LLPs depend on partnership agreements. If your goal is long-term growth and investment, an LLC might be the better option. If you prefer simplicity and internal control, an LLP could be ideal.

What is an LLP (Limited Liability Partnership)?

The concept of a Limited Liability Partnership emerged as a modern response to the limitations found in traditional partnerships and corporations. Initially introduced in the United States during the early 1990s, LLPs were designed to protect partners in professional firms—such as law and accounting—from being personally liable for the negligence or misconduct of another partner. Over time, the structure proved useful beyond professional services and was adopted by countries like the UK, India, Canada, and Australia.

An LLP is a hybrid structure that combines the operational flexibility of a general partnership with the liability protection of a corporation. In an LLP, two or more individuals can come together to manage a business while ensuring that their personal assets are shielded from the debts and obligations of the firm. This model aims to encourage collaboration without exposing individual partners to excessive risk.

Key Features of an LLP

One of the main features that makes LLPs attractive is limited liability. Each partner’s responsibility for the firm’s debts is limited to the amount they invest in the business. This is crucial for small businesses where risk management is a top priority, and it ensures personal assets remain protected unless there is misconduct or personal guarantees involved.

Another significant feature is that an LLP is a separate legal entity from its partners. This means the LLP can enter into contracts, own property, and initiate or face legal proceedings in its own name. This legal distinction enhances credibility and simplifies many aspects of doing business.

Is an LLP Best for a Small Business?

For many small businesses, particularly those offering services, LLPs provide a balance of protection and flexibility. They offer liability safeguards without the rigid structure of a corporation, allowing partners to manage internal operations through mutual agreement rather than strict statutory requirements. This can be very beneficial when forming a new business with friends or colleagues.

LLPs are particularly well-suited for service-based businesses like legal firms, accounting practices, consultancies, and design studios. These enterprises often rely on the combined expertise of their founders and don’t require venture capital investment, making the LLP structure ideal. However, it’s important to assess long-term goals to ensure the structure continues to meet the business’s needs.

Scenario: Service-Based Business

In service-based industries, LLPs provide the legal and financial protections needed to operate confidently. Law firms, consultancy agencies, and design studios can benefit from shared responsibilities while protecting individual partners from personal liability stemming from another partner’s actions. This makes it easier to collaborate without risking one’s personal finances.

Moreover, many professionals prefer LLPs due to the simplified tax structure and flexible profit-sharing. In industries where intellectual contribution is key, being able to allocate profits based on effort or expertise rather than capital contribution allows for more equitable partnerships.

Scenario: Product-Based Business

For product-based businesses, especially those involving manufacturing, inventory, or large-scale logistics, an LLP might not be the best option. These businesses often need external investment and may want to offer equity to attract investors, something not possible within the LLP framework. Corporations or LLCs may be better suited in such scenarios.

Additionally, product businesses usually scale rapidly and involve complex operations. The lack of formalized hierarchy in LLPs may create challenges in decision-making and governance. For long-term scalability and outside investment, transitioning to a different structure might become necessary.

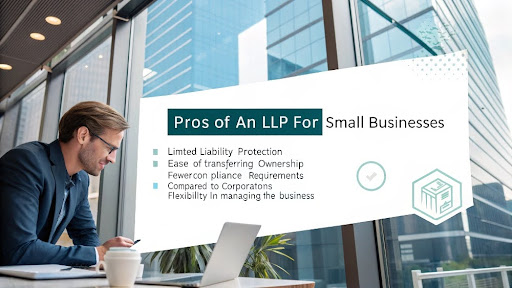

Pros of an LLP for Small Businesses

Liability protection is perhaps the most compelling advantage. LLPs ensure that one partner is not held responsible for another’s misconduct. This protection creates a secure environment, especially for small businesses that involve multiple stakeholders. It allows each partner to focus on their strengths without fearing personal financial ruin.

Another major benefit is the absence of double taxation. Profits pass directly to the partners, who report them on personal tax returns. This eliminates the burden of paying both corporate tax and personal income tax on the same earnings, which is often a concern with corporations.

More Advantages of an LLP

LLPs offer customized profit-sharing agreements, meaning partners can divide income based on skill, effort, or capital rather than equally. This allows for more personalized and practical compensation models that reflect real contributions.

They also come with lower compliance requirements compared to corporations. With fewer formal meetings, reporting obligations, and bureaucratic procedures, partners can spend more time focusing on growing the business rather than meeting government deadlines.

Cons of an LLP for Small Businesses

Despite their advantages, LLPs aren’t perfect. One key drawback is limited global recognition. Some countries do not recognize LLPs, and in cross-border operations, this can lead to complications or restrictions when expanding internationally.

LLPs also cannot issue shares, making it nearly impossible to bring in equity investors. If your small business plans to seek venture capital or angel investment, this structure will likely hinder those opportunities. Investors typically prefer structures like LLCs or corporations that can accommodate equity stakes.

More Drawbacks of an LLP

Public disclosure requirements can also be a disadvantage. In certain countries, LLPs must file financial statements, which become public records. Some small business owners may see this as an intrusion into their private affairs.

Ownership transfer in LLPs can be complex and time-consuming. Unlike corporations, where shares can be sold or transferred easily, changing partners in an LLP usually requires amending the partnership agreement, which can be legally and operationally cumbersome.

Taxation in an LLP

LLPs generally benefit from pass-through taxation, meaning the business itself isn’t taxed on profits. Instead, individual partners report their share of income or losses on their personal tax returns. This system can lead to substantial tax savings, especially when profits are modest in the early years.

However, partners are often considered self-employed and must pay self-employment taxes. In countries like the U.S., this includes Social Security and Medicare contributions. Understanding these obligations helps avoid surprises during tax season and allows better financial planning.

When is an LLP Not a Good Option?

If your business model involves seeking large-scale investment or going public, LLPs are not suitable. Since LLPs can’t issue shares or easily accept outside investors, this makes them a poor fit for startups aiming for rapid growth and capital infusion.

Another scenario where LLPs fall short is in businesses with frequent ownership changes. Transferring ownership requires significant legal effort and may disrupt operations. In contrast, LLCs and corporations allow for smoother ownership transitions.

Jurisdictional Considerations

In the United States, each state has unique rules about LLP formation and eligibility. For instance, California restricts LLPs to licensed professionals such as lawyers and accountants. This could limit your options depending on your business model and location.

In the United Kingdom, LLPs must file annual accounts and are regulated by Companies House. While this ensures transparency, it also means more formal requirements. In India and Australia, LLPs are viable but come with specific compliance and filing expectations.

Steps to Register an LLP

First, choose a business name that is distinct and includes “LLP” at the end to reflect your entity type. This name must not infringe on existing trademarks and should follow naming guidelines provided by the business registry.

Next, draft a comprehensive LLP agreement. This legal document outlines partner roles, responsibilities, capital contributions, profit-sharing, and rules for dispute resolution. It serves as the backbone of your partnership and helps prevent conflicts.

Completing the Registration

File the appropriate forms with your country or state’s corporate affairs office or equivalent. These forms typically include partner details, office address, and the signed LLP agreement. This step officially registers your LLP as a separate legal entity.

Finally, secure all required business licenses and tax registrations. Depending on your industry and jurisdiction, you may need local permits, sales tax registration, or VAT/GST numbers. Ensure full compliance before launching operations.

Real-World Case Studies

A law firm in New York chose to form an LLP due to the professional nature of its work and the desire for shared responsibility. The partners benefited from the LLP’s liability protection, flexible management, and equitable profit-sharing. It also allowed for conflict resolution without extensive legal intervention, thanks to a strong partnership agreement.

In contrast, a California-based software consultancy initially registered as an LLP but later transitioned to an LLC when venture capital became essential. Investors required equity, which the LLP structure couldn’t provide. The switch allowed the company to scale and attract funding.

Additional Case Examples

An accounting firm in London adopted the LLP model to combine its partners’ expertise while minimizing administrative overhead. The structure enhanced their professional credibility and attracted senior talent looking for a stake in the business without unnecessary bureaucracy.

Another example is a group of management consultants in Toronto who selected the LLP model due to its simplified compliance and strong internal control. Their business grew steadily, focusing on long-term client relationships without needing outside capital.

Final Verdict

Conclusion:

An LLP can be a great fit for small businesses focused on internal control and professional services. However, if your business goals include scaling, attracting investors, or forming in a business-friendly state like California, an LLC might be the smarter move.

Here’s a step-by-step guide on how to start an LLC in California if you’re considering this structure for your business.